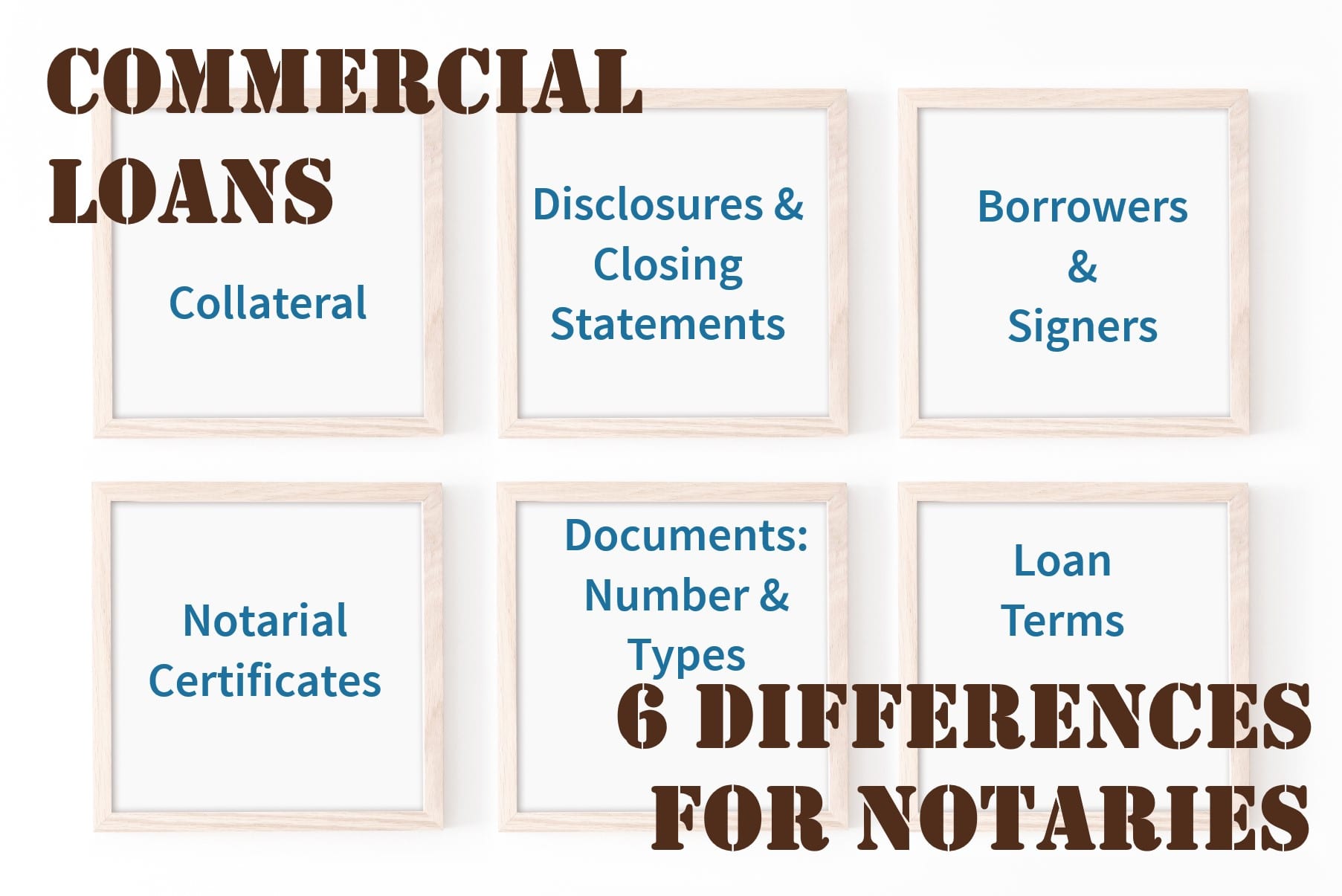

Commercial Mortgage Loans: Six Differences for Notary Signing Agents

Last week we reviewed nine typical loan packages and discussed the sizes of each and the estimated number of notarial acts. There are a few loan types that are significantly different than the others, the commercial mortgage loan being the most different. The topic of commercial loans is also quite popular with new notaries. With that in mind, this week, we are going to cover the six primary differences that notaries need to know about when switching over from residential loans to handling commercial loans.

1-Collateral

Collateral means the type of property that secures the loan. The collateral seen by notaries in residential loans are homes or land on which a home will be constructed. The home may be a standalone one-family house or a multifamily property of one to four units. Any multifamily property having over four units falls into the commercial mortgage loan category.

When dealing with commercial mortgages, notaries will see these six types of real property (or the raw land on which one of these types will be built):

- Office buildings

- Multifamily with 5+ units

- Industrial

- Hotel

- Retail

- Special Purpose

In other words, notaries will see collateral ranging from raw land to hire rise offices, hotels to hospitals, bed and breakfast businesses to car dealerships, government buildings to charity clinics, and many others. Notably, furniture and fixtures may also be included as collateral to secure commercial loans.

2- Disclosures and Closing Statements

Disclosures that commercial borrowers are provided early on are few, generally speaking, unless part of the homestead is included as collateral.

Residential borrowers receive tons of disclosure paper before moving forward on a residential loan.

In a commercial mortgage, the closing statement is different, too. On a residential loan, the statement must be a Closing Disclosure. For a commercial property, there will be something that looks like a HUD 1 Settlement Statement, or an actual HUD 1 form. In fact, the closing statement can be a complex list of closing costs typed informally on letterhead, or even on a piece of plain paper. In other words, commercial mortgages are not regulated as tightly as residential mortgages are.

3-Borrowers / Signers

Signers in all loans are people, of course. In all loans, their personal names will appear in the documentation. In residential mortgage loans, the signers are the borrowers and they sign as individuals. However, borrowers in commercial loans are entities. In commercial mortgages, the signers who appear at the appointment to sign will have been granted signing authority by the borrowing entity. (Entities are forms of business, e.g., corporations, limited liability companies, government agencies, non-profit organizations, even sole-proprietors, to name a few.) There will often be more signers at the table.

4-Notarial Certificates

In residential mortgages, the notarial certificates state the names of people as individuals. In commercial work, you will need to know how to complete jurats and certificates of acknowledgements that have the names of entities in addition to the person who appeared before you. Previously, I wrote an article for notaries called 5-Step Plan to Master Complicated Certificates. Please refer to it for more information on how to handle those types of certificates.

5- Documents: Number and Types

Standard document packages are 100 – 150 pages in most of the packages mentioned in last weeks article. However, 500 pages is not uncommon in a commercial loan document package. You will also see documents that will be unfamiliar to you. Well-trained notaries can handle any document’s notarization. That is why all notaries who handle loans of any type need training and should refresh their training every few months. I want to encourage every reader to please take a notary class and become trained before handling loan document packages. It protects you! It makes you stand out as a professional! There are no better training classes than right here on Notary.net! The price is right and the materials are superior.

6-Loan Terms

The interest rates are often a little higher. In standard residential packages, notaries see that the loan length is 15, 20, or 30 years. In a commercial mortgage, the loan might be for financed for eight years and the amortization is based on 20 years. ANYTHING is possible.

Next Week – More Commercial Mortgage Insights!

Next week’s article will be “How Notaries Can Prepare to Handle Commercial Mortgage Loans.” The article will cover the core documents of a commercial mortgage loan and other ways notaries can prepare to be ready for commercial lending packages.

Personal Message

I didn’t give proper credit for my previous article. I had help. Jake Burkhalter is a friend who recently retired from a 22+ year career entailing escrow. The information from the article on loan package types last week was influenced heavily by input by Jake Burkhalter and I forgot to mention this. In fact, as my friend, Jake often looks over my work to make sure I am in harmony with what title companies look for in signing agent procedures. His insights and assistance have been invaluable to me in my growth as a writer for notaries and in me being able to provide insight to new notaries about the nuts and bolts of being a great notary and notary signing agent.

Share this post

Leave a Reply

You must be logged in to post a comment.

Comments (3)

Brenda,

This is great. Thanks for sharing!

Thanks so much “clewis”!

Awesome information. Thanks for sharing!