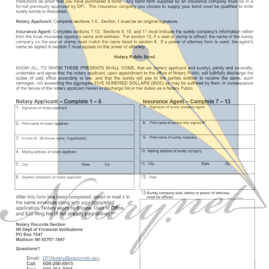

Notary Surety Bonds

Notary bonds protect the public from any mistake you might make while fulfilling your notarial duties. Notary surety bonds required in many states. If your actions result in harm to the public, a claim can be made on the bond. If a valid claim is made on the bond, the surety company will pay the claim and you will be required to reimburse them. In California, for example, the bond limit is $15,000, and that money would come out of your pocket.

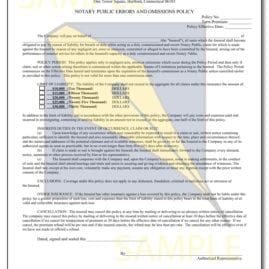

The good news is that a notary errors and omissions (E&O) policy will step in to defend you. If you have this type of policy, it could pay the claim on your behalf, protecting your assets in the process.

-

Select options This product has multiple variants. The options may be chosen on the product pageQuick ViewMissouri, Missouri Notary Bonds and Insurance, Notary Bonds

Select options This product has multiple variants. The options may be chosen on the product pageQuick ViewMissouri, Missouri Notary Bonds and Insurance, Notary BondsMissouri Notary Bond + Free E&O Insurance

$30.00Missouri notaries are required by state law to have a 4 year, $10,000 Missouri notary bond. The Missouri notary surety bond protects the people of Missouri from any mistakes you…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

Notary Bonds, Pennsylvania, Pennsylvania Notary Bonds & E&O

Notary Bonds, Pennsylvania, Pennsylvania Notary Bonds & E&OPennsylvania Notary Surety Bond – Travelers

$30.00Pennsylvania notaries are required by state law to have a 4 year, $10,000 Pennsylvania notary bond. The Pennsylvania notary surety bond protects the people of Pennsylvania from any mistakes you…

-

Select options This product has multiple variants. The options may be chosen on the product pageQuick ViewNotary Bonds, Texas, Texas Bonds and E&O Insurance

Select options This product has multiple variants. The options may be chosen on the product pageQuick ViewNotary Bonds, Texas, Texas Bonds and E&O InsuranceTexas Notary Bond

$50.00Texas Notary Bond

Texas notaries are required by state law to have a 4 year, $10,000 Texas notary bond. The Texas notary surety bond & notary application is required to become…Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

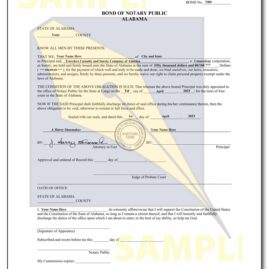

Select options This product has multiple variants. The options may be chosen on the product pageQuick ViewAlabama, Alabama Notary Bonds and E&O Insurance, Notary Bonds

Select options This product has multiple variants. The options may be chosen on the product pageQuick ViewAlabama, Alabama Notary Bonds and E&O Insurance, Notary Bonds4-Year, $50,000 Alabama Notary Bond

$50.00Alabama notaries are required by law to maintain a $50,000 notary bond for the duration of their 4-year commission. The Alabama notary bond protects the people of Alabama from any…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

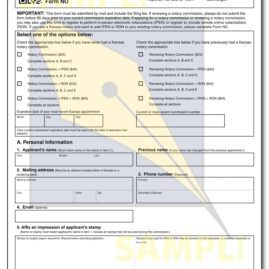

Kansas, Kansas Notary Bonds & Insurance, Notary Bonds

Kansas, Kansas Notary Bonds & Insurance, Notary BondsKansas Notary Bond

$30.00Kansas Notary Bond

Notaries in Kansas are required by law to have a $12,000, 4-year Kansas notary bond. The Kansas notary bond protects the people of Kansas from any mistakes a… -

Notary Bonds, Wisconsin, Wisconsin Notary Bonds & Insurance

Notary Bonds, Wisconsin, Wisconsin Notary Bonds & InsuranceWisconsin Notary Surety Bond

$20.00Wisconsin Notary Bond

Wisconsin law requires all notaries to purchase and maintain a $500 notary surety bond for the duration of their commission. The Wisconsin notary bond protects the people of… -

Select options This product has multiple variants. The options may be chosen on the product pageQuick ViewArizona, Arizona Notary Bonds and Insurance, Notary Bonds

Select options This product has multiple variants. The options may be chosen on the product pageQuick ViewArizona, Arizona Notary Bonds and Insurance, Notary BondsArizona Notary Surety Bond

$25.00An Arizona notary is required by state law to have a 4 year $5,000 Arizona notary bond. The Arizona notary surety bond protects the people of Arizona from any mistakes…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

California, California Notary Bonds and E&O Insurance, Notary Bonds

California, California Notary Bonds and E&O Insurance, Notary BondsCalifornia Notary Surety Bond – Travelers

$38.00California Notary Bond

Notaries in California are required by law to have a 4 year, $15,000 California notary bond. The California notary bond protects the people of California from any mistakes…