Notary Bonds & Insurance

Notaries are required to be bonded in approximately 30 states. A notary surety bond protects the public from mistakes the notary makes that result in harm to others. In those instances, a claim can be made against the bond. Errors and omissions insurance, on the other hand, protects that notary subject to policy terms and conditions.

The differences between a notary bond and errors and omissions insurance is important to understand. In short, a notary bond protects the public; notary errors and omissions insurance protects you.

Notaries often provide other services: tax preparation, service of process, vehicle registration, legal document assistant services, immigration consulting services, and more. The Other Surety Bonds category includes a variety of additional bonds a notary public may need.

-

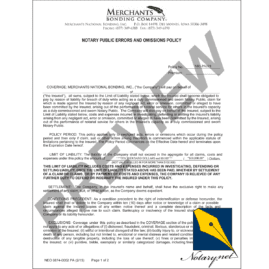

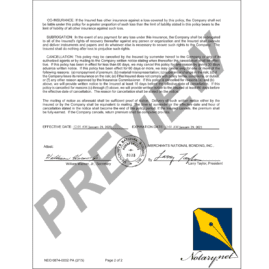

Errors & Omissions

50 products

-

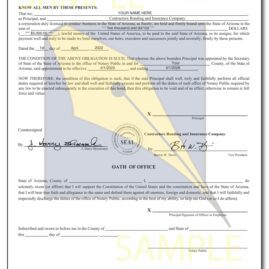

Notary Bonds

30 products

-

Alaska, Alaska Notary Bonds and E&O Insurance, Errors & Omissions

Alaska, Alaska Notary Bonds and E&O Insurance, Errors & OmissionsAlaska Notary E&O Insurance

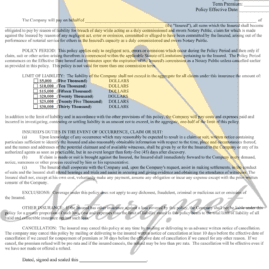

$16.25 – $416.00Alaska Notary Errors and Omissions Insurance. Our policies range from $10,000 to $100,000 to cover you for your current commission term. Errors and Omissions Insurance helps protect you, the notary…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

Arizona, Arizona Notary Bonds and Insurance, Errors & Omissions, Notary Bonds & Insurance

Arizona Notary E&O Insurance

$13.00 – $416.00An Arizona Notary Errors and Omissions Insurance policy can help protect you from claims made against you for making a mistake on a notarial act. Choose your coverage term and…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

Arkansas, Arkansas Notary Bonds and E&O, Errors & Omissions

Arkansas Notary E&O Insurance

$130.00 – $832.00Arkansas Notary Errors and Omissions policies range from $10,000 to $100,000 and can be purchased to cover you for the duration of your current commission term.

Notary bonds and E&O policies…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

Colorado, Colorado Notary Bonds & Insurance, Errors & Omissions

Colorado Notary E&O Insurance

$13.00 – $416.00Please select your desired term and coverage amount. For Colorado notary applicants or new Colorado notaries, we recommend selecting the full 4-year term for coverage as long as you hold…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

Connecticut, Connecticut Notary Bonds & Insurance, Errors & Omissions

Connecticut Notary E&O Insurance

$16.25 – $520.00Connecticut Notary Errors and Omissions Insurance. Our policies range from $10,000 to $100,000 and can be purchased for 1-5 year term limits. Errors and Omissions Insurance helps protect you, the…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

Delaware, Delaware Notary Bonds & Insurance, Errors & Omissions

Delaware Notary E&O Insurance

$16.25 – $416.00Delaware Notary Errors and Omissions Insurance policies range from $10,000 to $100,000 and can be purchased for 1-4 year term limits. Errors and Omissions Insurance helps protect you, the notary…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

Errors & Omissions, Florida, Florida Notary Bonds & Insurance

Florida Notary E&O Insurance

$25.00 – $240.00Florida Notary Errors and Omissions Insurance policies range from $5,000 to $100,000 and cover you for the term of your commission.. Errors and Omissions Insurance helps protect you, the notary…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

Errors & Omissions, Georgia, Georgia Notary Bonds & Insurance

Georgia Notary E&O Insurance

$13.69 – $350.50Georgia Notary Errors and Omissions Insurance policies range from $10,000 to $100,000 and can be purchased for 1-4 year term limits. Errors and Omissions Insurance helps protect you, the notary…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View -

Errors & Omissions, Hawaii, Hawaii Notary Bonds & Insurance

Hawaii Notary E&O Insurance

$7.75 – $1,040.00Hawaii Notary Errors and Omissions Insurance policies range from $5,000 to $100,000 and can be purchased for 1-5 year term limits. Errors and Omissions Insurance helps protect you, the notary…

Select options This product has multiple variants. The options may be chosen on the product pageQuick View